Simple Formula to Calculate Home Loan EMI

Understanding how EMI is derived helps borrowers see how long-term repayment commitments are structured. Even though calculators provide instant answers, knowing the underlying formula gives clarity on how loan amount, interest rate, and tenure interact.

A simple method for calculating home loan is to use the EMI formula based on loan amount, interest rate, and tenure to estimate your monthly repayment. This helps interpret repayment in a more structured way instead of relying only on automated outputs.

Why Understanding the EMI Formula Matters

The EMI formula is often skipped by borrowers who rely fully on digital tools, but understanding it provides financial clarity.

- Transparency in repayment: Knowing how EMI is calculated helps explain changes in instalments due to tenure or interest rate variations. This improves clarity on repayment structure.

- Better financial planning: It becomes easier to estimate how loan decisions may affect long-term cash flow. This supports more structured financial planning.

- Independent understanding: Familiarity with EMI calculations allows borrowers to interpret figures without relying entirely on external tools. This improves overall financial awareness.

This basic awareness helps in evaluating loan structures more confidently.

The Standard EMI Formula Explained

EMI calculation is based on a mathematical structure that distributes repayment across principal and interest over time.

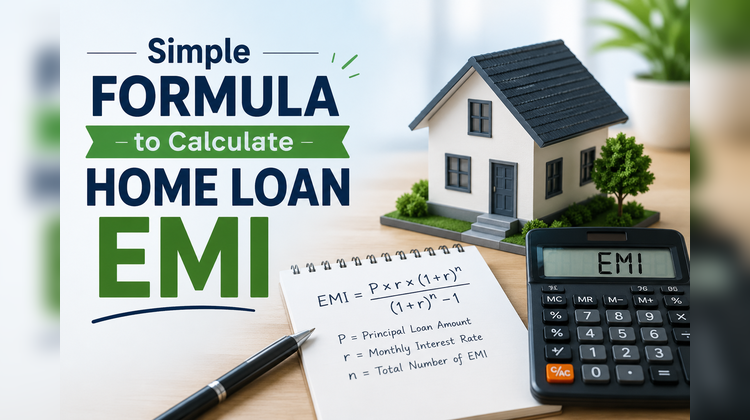

- Formula representation: EMI = P × r × (1 + r)ⁿ / [(1 + r)ⁿ − 1]

- P (Principal): The total loan amount borrowed from the lender.

- r (Monthly interest rate): Annual interest divided by 12 and converted into decimal form.

- n (Number of months): Total repayment tenure expressed in monthly instalments.

This formula ensures a consistent EMI across the loan period while balancing interest and principal repayment.

How Each Factor Influences EMI Value

Each component of the formula plays a different role in determining the final monthly repayment amount.

- Loan amount impact: A higher principal increases the EMI, as repayment is calculated on the total borrowed amount. This directly affects monthly outflow.

- Interest rate effect: Even small changes in interest rates can impact total repayment over time. This influences both EMI size and overall cost.

- Tenure influence: Longer tenures reduce EMI amounts but increase total interest paid. Shorter tenures have the opposite effect.

A home loan can be calculated using a simple formula based on the loan amount, interest rate, and repayment tenure to understand the total repayment cost. This relationship between variables determines affordability and long-term financial load.

Using the Formula for Scenario Analysis

The formula is not just for calculation, it can also be used to compare different borrowing options.

- Tenure comparison: Different repayment periods result in varying EMI amounts and total interest paid. Shorter tenures increase EMIs but reduce overall cost, while longer tenures do the opposite.

- Interest sensitivity: Even small changes in interest rates can affect EMIs and total repayment. This shows how borrowing costs can fluctuate over time.

- Repayment planning: Evaluating different scenarios helps understand how prepayments may reduce future interest burden and alter loan duration.

Scenario-based understanding allows better visibility into long-term financial outcomes.

Common Mistakes in EMI Estimation

Incorrect assumptions can lead to misleading EMI expectations even when the formula is known.

- Wrong rate conversion: Not converting annual interest into a monthly rate can distort EMI calculations. This leads to inaccurate repayment estimates.

- Ignoring compounding effect: Interest is calculated on a reducing balance basis, not a flat rate. Overlooking this can misrepresent actual interest out-go.

- Focusing only on EMI size: Lower EMIs may seem easier to manage but can increase total repayment. This happens due to longer tenure and higher cumulative interest.

Accurate inputs are essential for meaningful EMI estimation.

Manual Calculation vs Digital Tools

Both manual and digital methods serve different purposes in EMI planning.

- Manual calculation: Working through EMI formulas helps build a clear understanding of how principal, interest, and tenure interact. This improves conceptual clarity.

- Digital calculators: Online tools provide quick results for different scenarios. They simplify comparison without requiring detailed calculations.

- Error reduction: Automated tools minimise calculation errors, especially in complex formulas. This improves accuracy in estimating EMIs and total repayment.

A balanced approach using both methods improves clarity and efficiency in loan planning.

Conclusion

Understanding the EMI formula explains how loan amount, interest rate, and tenure combine to shape monthly repayments and total cost. This clarity helps interpret calculator outputs and compare different repayment scenarios more logically. Calculating home loan EMI through both formula-based understanding and digital tools provides a clearer view of repayment structure, affordability limits, and how long-term financial commitments are distributed over the loan tenure.

NOTE: No TechCircle Journalist was involved in the creation/production of this content.

Next Article